I. Price as Probability: The Economic Foundation of Prediction Markets

The most fundamental economic principle behind prediction markets is simple: A contract’s price reflects the market’s estimated probability of an event occurring.

Examples:

- A “Yes” contract trading at 0.62 implies the market believes the event has roughly a 62% chance of happening.

While this may seem like a strong assumption, it has been repeatedly validated across real-world cases—including elections, policy outcomes, sports events, and on-chain milestones.

Why Can Price Represent Probability?

This works because of three reinforcing forces:

1. Real financial incentives drive honest signaling

- Prices in prediction markets are not opinions or polls—they are backed by capital.

- Incorrect probability assessments result in direct financial losses.

2. Continuous trading naturally corrects mispricing: When prices deviate from collective expectations, traders step in to buy undervalued contracts or sell overpriced ones. This arbitrage behavior constantly pulls prices back toward the market’s true consensus.

3. Markets aggregate distributed information: Each participant holds different information, insights, or beliefs. The market combines these fragmented signals into a single, public price that reflects collective knowledge.

At its core, prediction market mechanism design focuses on enabling prices to adjust faster, become more accurate, and remain difficult to manipulate.

2. Order Book Model: A Prediction Market Built on Traditional Market Structure

The order book model is the prediction market design most closely aligned with traditional financial exchanges. Prices are formed through limit orders and matching.

In a prediction market, an order book works much like spot or options trading:

- Buyers place bids to purchase Yes/No contracts

- Sellers place offers to sell

- Trades execute when bid and ask prices cross

- The market price is determined by the most recent trade

Advantage

- Precise price discovery: Prices emerge directly from trader competition, reflecting real-time supply and demand.

- Better execution for large trades: Participants can split orders and avoid the slippage often seen in AMM curves.

- Familiar to professional traders: Strategies such as arbitrage, market making, and hedging can be applied with minimal adaptation.

Limitations

- Liquidity depends on active market makers: Without sufficient participation, order books become shallow and volatile.

- Early-stage markets often lack depth: This can lead to wide spreads, and aggressive order sweeping.

- Prices update discretely, not continuously: This makes order books less suitable for use cases that require smooth, real-time probability signals (e.g., on-chain queries).

When the Order Book Model Works Best

- Major events with long time horizons and consistent capital participation

- Markets dominated by professional traders

- Ongoing market-making support from institutions (e.g., Kalshi)

The order book model is better suited to institutional-grade prediction markets rather than being a purely Web3-native design.

III. The AMM Model: A Core Innovation of Web3 Prediction Markets

On-chain, traditional order books struggle to rely on high-frequency matching and deep liquidity. As a result, automated market maker (AMM) models have become the dominant design for prediction markets. Among them, the most important is LMSR (Logarithmic Market Scoring Rule), proposed by Robin Hanson, which serves as the mathematical foundation of on-chain prediction markets.

The Core LMSR Formula

LMSR determines market prices through a cost function:

C(q) = b · ln(e^(q₁/b) + e^(q₂/b))

Where:

- q₁, q₂ = quantities of the Yes and No contracts

- b = liquidity parameter (controls price sensitivity and slippage)

Prices are derived from the partial derivative of the cost function:

P(Yes) = e^(q₁/b) / (e^(q₁/b) + e^(q₂/b))

This creates a smooth, continuous market-making curve that guarantees liquidity at all times.

Advantages of the AMM Model

- Always provides liquidity (no “can’t buy” or “can’t sell” situations)

- Continuous pricing that can be interpreted as real-time probability

- On-chain computation–friendly

- Market stability can be tuned by adjusting the b parameter.

Limitations of the AMM Model

- Large trades can cause significant price slippage

- Early large capital participants may influence prices (though at a high cost)

- Liquidity provider incentives are required; otherwise, the cost curve lacks sufficient depth.

Why the b Parameter Matters

- Smaller b → Prices are highly sensitive; even small trades can significantly move probabilities.

- Larger b → Prices are more stable, making it better suited for major, long-horizon events.

This is why Web3 prediction markets often adjust curve parameters based on the type of event.

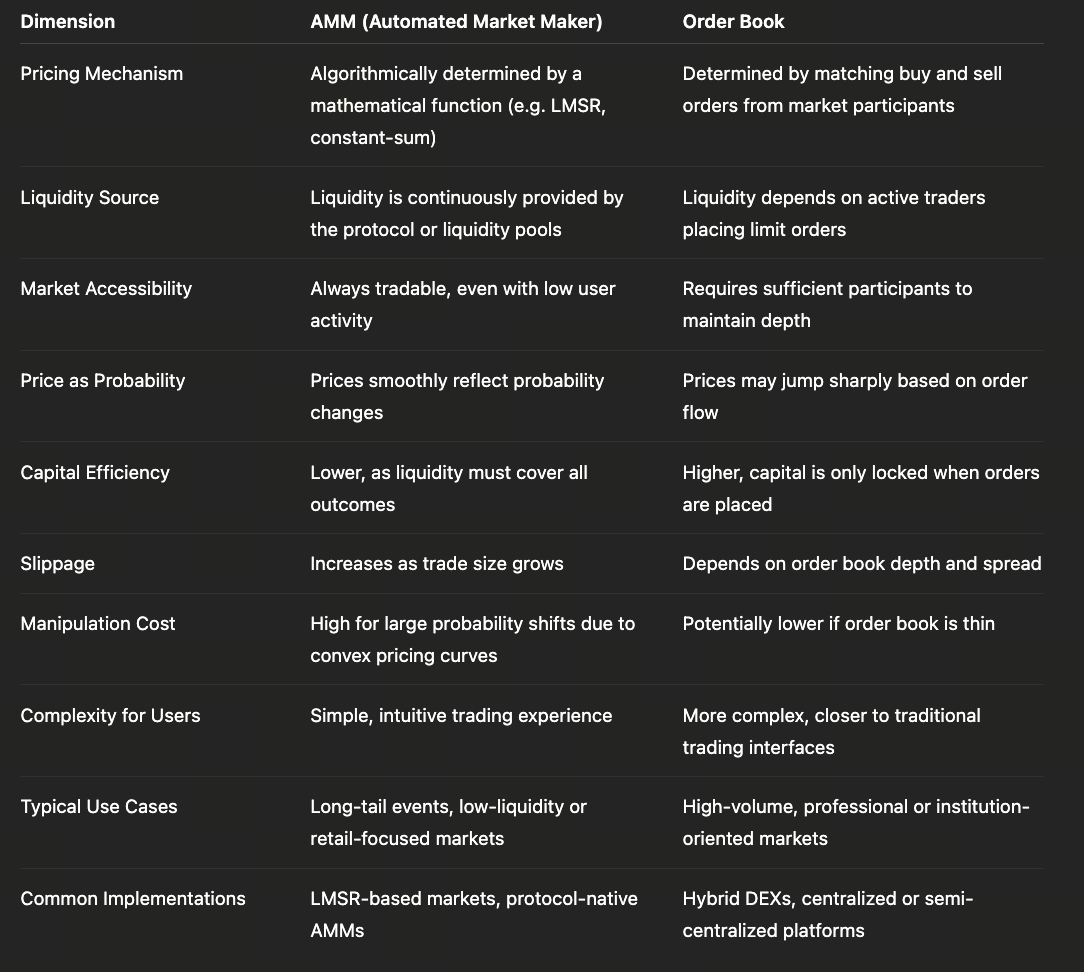

IV. AMM vs. Order Books: A Comparison of Two Market Models

The distinction between AMMs and order books is not merely technical. Rather, they represent two different economic choices for prediction markets at different stages of development and with different user structures. The core advantage of AMMs lies in continuous tradability. Even when market participation is low or event attention is limited, an algorithmic pricing mechanism can still provide quotes, allowing prediction markets to cover a wide range of long-tail events. This design makes AMMs a critical tool for early-stage market expansion and for lowering participation barriers. The trade-off, however, is that capital must be pre-allocated across all possible outcomes, resulting in lower capital efficiency and amplified non-linear price effects during large trades.

In contrast, the order book model aligns more closely with traditional financial market price discovery, where prices are determined entirely by the interaction of buyers and sellers. Capital is only committed when actual orders are placed, making the model more capital-efficient and better at conveying clear supply-and-demand signals for high-participation events. However, order books are highly sensitive to liquidity conditions: as participation declines and order depth thins, price volatility and manipulation risk increase significantly. This limits their practicality for long-tail prediction events.

From a longer-term perspective, AMMs and order books are not opposing designs, but complementary components within the lifecycle of prediction markets. AMMs function as a “bootstrapping mechanism,” ensuring markets remain operable in their early stages, while order books represent a more “mature state,” taking over price discovery as consensus consolidates and trading demand grows. As a result, an increasing number of prediction markets are exploring hybrid models—using AMMs to provide baseline liquidity and continuous pricing, while leveraging order books to support high-frequency trading and large capital flows. This evolutionary path reflects a natural transition for prediction markets from prioritizing accessibility toward prioritizing efficiency and depth.

V. Game Design in Prediction Markets: Manipulation Costs, Arbitrage, and Price Correction

Prediction markets differ fundamentally from traditional financial assets, as they operate under a distinct game-theoretic economic design. For a prediction market to remain healthy, several key conditions must be met.

1. High Cost of Manipulation

Example:

- Pushing the probability of a “Yes” outcome from 60% to 90% requires purchasing a large volume of “Yes” contracts.

- If the event ultimately fails to occur, the manipulator incurs a total loss.

As a result, manipulation is extremely costly and cannot be unwound in the same way as price pumping in traditional markets. This characteristic gives prediction markets a high degree of credibility, particularly in political and policy-related events.

2. Arbitrage Mechanisms Automatically Correct Prices

Common forms of arbitrage in prediction markets include:

- Cross-platform arbitrage (the same event priced differently across markets)

- Cross-contract arbitrage (e.g., Yes/No arbitrage)

- Structural arbitrage (e.g., inconsistencies between the probabilities of parent events and their sub-events)

Arbitrageurs continuously eliminate pricing errors, driving market prices closer to true probabilities.

3. Information Is Immediately Reflected in Prices

News, leaks, and social media sentiment can all trigger rapid price movements. Prediction markets are highly information-sensitive systems.

Example:

- A single statement during a regulatory hearing

- A crypto project delaying its mainnet launch

- Changes in a political candidate’s health

Each of these can cause abrupt price shifts that instantly reflect updated market consensus.

VI. How Mechanism Design Shapes a Prediction Market’s Ecosystem

Different prediction market platforms adopt different mechanism designs, which directly shape their strengths and positioning:

- AMM-based models: Best suited for a large number of small or niche events, with strong coverage of long-tail scenarios

- Order book–based models: Ideal for high-participation events with strong public attention

- Hybrid models (currently being explored by some platforms): Combine an AMM as a liquidity foundation with order books to add depth and support larger trades

Mechanism design ultimately determines:

- The tradability of events

- User experience

- A platform’s ability to scale

- The range of strategies available to investors (arbitrage, hedging, long-term positioning, etc.)

Understanding these mechanisms can also help identify which platforms are more likely to succeed in the future.