Author: Nancy, PANews

Bitcoin quietly recorded eight consecutive days of gains amid the smoke of Middle East conflicts, with the world’s largest Bitcoin strategy using real money to fuel this round of rebound with a blazing fire.

Half a month ago, Strategy (MicroStrategy) suddenly stepped on the accelerator, finally turning Bitcoin positions from losses to profits. In just one week, it accumulated over 40,000 Bitcoin, spending more than $2.8 billion. The size of this capital exceeds the net inflow into Bitcoin ETFs during the same period.

Behind Strategy’s vigorous activity, nearly half of the funds come from perpetual preferred stock STRC, contributing over 20,000 Bitcoin to the treasury. This financing tool, focused on stable returns, successfully packages highly volatile Bitcoin into a fixed-income product favored by traditional finance, continuously attracting funds from Wall Street and becoming a new growth engine for Strategy.

Single-day purchase volume exceeds five times the entire network output, making STRC a new financing weapon

In just a few months since its launch, STRC has transformed from an innovative tool into a powerful financing weapon in Strategy’s arsenal.

Data from STRC.live shows that since its launch in July 2025, STRC has issued 10 ATM (at-the-market) offerings, selling over 50.25 million units, injecting approximately 50,792 Bitcoin into Strategy’s treasury over eight months—equivalent to about $4.74 billion.

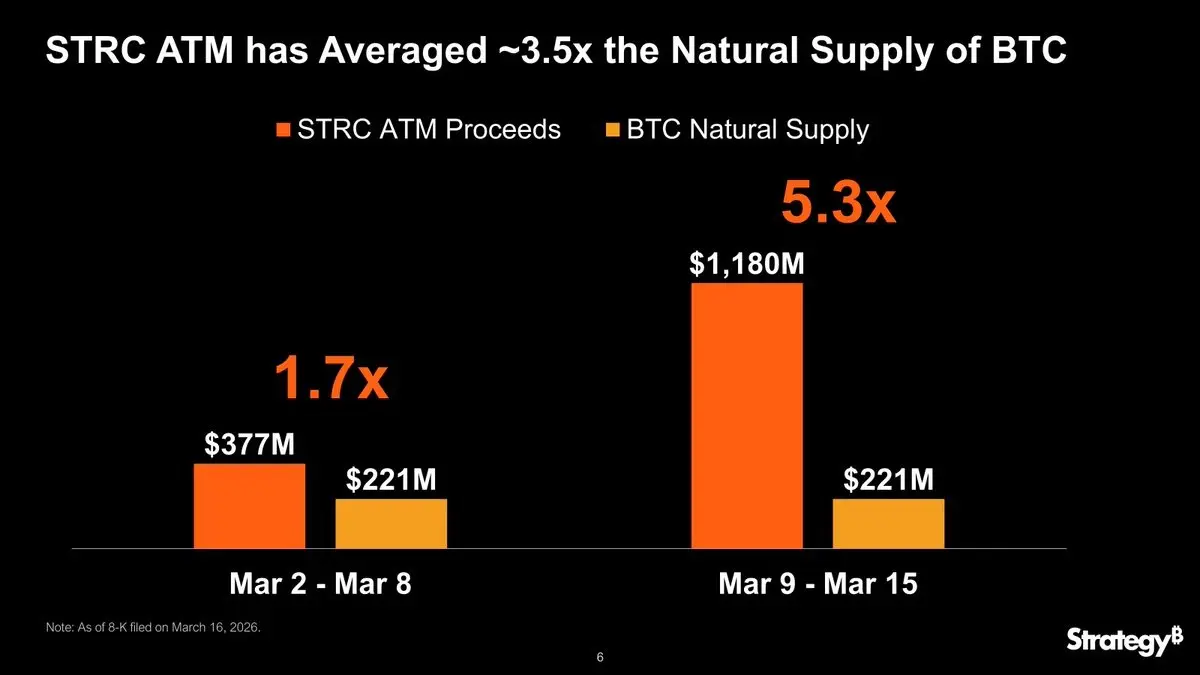

Especially in the past week, STRC contributed about 22,000 Bitcoin, accounting for 43.5% of the overall increase during that period, representing 54.8% of Strategy’s net increase. On March 9, it funded the purchase of 5,315 Bitcoin, equivalent to 1.7 times the total network mining output during the same period; on March 16, it reached 16,816 Bitcoin, about 5.3 times the network’s total production.

In fact, during this year’s sideways or even declining Bitcoin prices, demand for STRC has been rising.

As of March 18, STRC’s market cap exceeded $5.02 billion, up $2.08 billion from the end of last year, a 58.5% increase. From a trading perspective, after March began, daily trading volume of STRC rapidly expanded, once exceeding $740 million in a single day. Between March 9 and 13 alone, total trading volume reached $2.3 billion, with about 86% of transactions above $100.

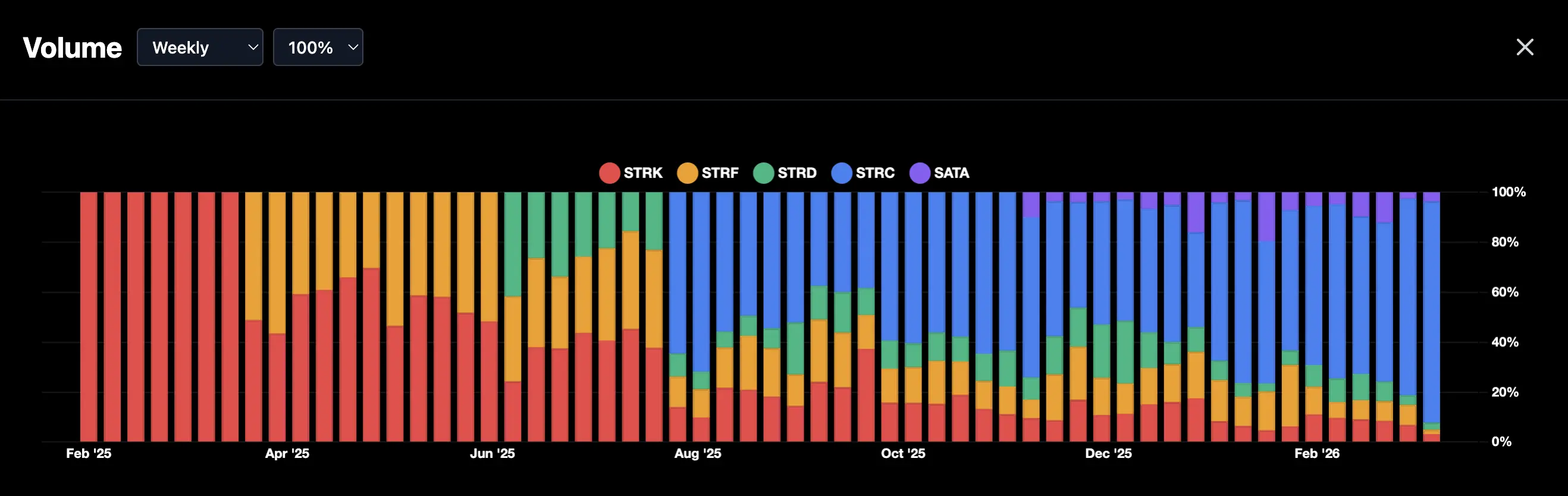

STRC’s performance far surpasses other similar products. Data from BitcoinQuant shows that over the past 30 days, STRC’s trading volume exceeded $150 million, significantly higher than products like STRK, SATA, and STRF; weekly trading share also climbed from a low of 37.5% to 88.5%.

Strategy CEO Michael Saylor recently stated that STRC is currently the most liquid preferred stock in the market. Strategy’s head of strategy, Chaitanya Jain, admitted that STRC and MSTR will together form the “ultimate Bitcoin accumulation machine.”

This model has also attracted DAT (cryptocurrency treasury) companies and traditional financial institutions to “get on board,” including DAT firms like Strive, Prevalon Energy, Anchorage Digital, and OranjeBTC, as well as funds under BlackRock, Fidelity, Virtus InfraCap, and John Hancock, all holding STRC.

From arbitrage premiums to yield games, Strategy’s dual ATM magic

The popularity of STRC essentially stems from Strategy packaging Bitcoin into a fixed-income product more aligned with traditional finance preferences.

This product, already listed on Nasdaq, can be traded directly through mainstream brokers. Unlike ordinary shares like MSTR, STRC is a floating-rate perpetual preferred stock designed to stay as close as possible to a $100 face value.

The implementation is straightforward: by dynamically adjusting dividend rates each month to anchor the price. Specifically, when STRC trades at or above $100, Strategy initiates an ATM offering, selling new shares and buying Bitcoin; when the price falls below $100, it increases dividends to boost attractiveness and pull the price back toward par.

This mechanism significantly reduces volatility. Official data shows that STRC’s historical volatility is about 14%, and over the past 30 days, it’s only 1.5%, much milder than Bitcoin or MSTR.

Meanwhile, monthly cash dividends are one of STRC’s biggest selling points, especially suitable for investors seeking stable income.

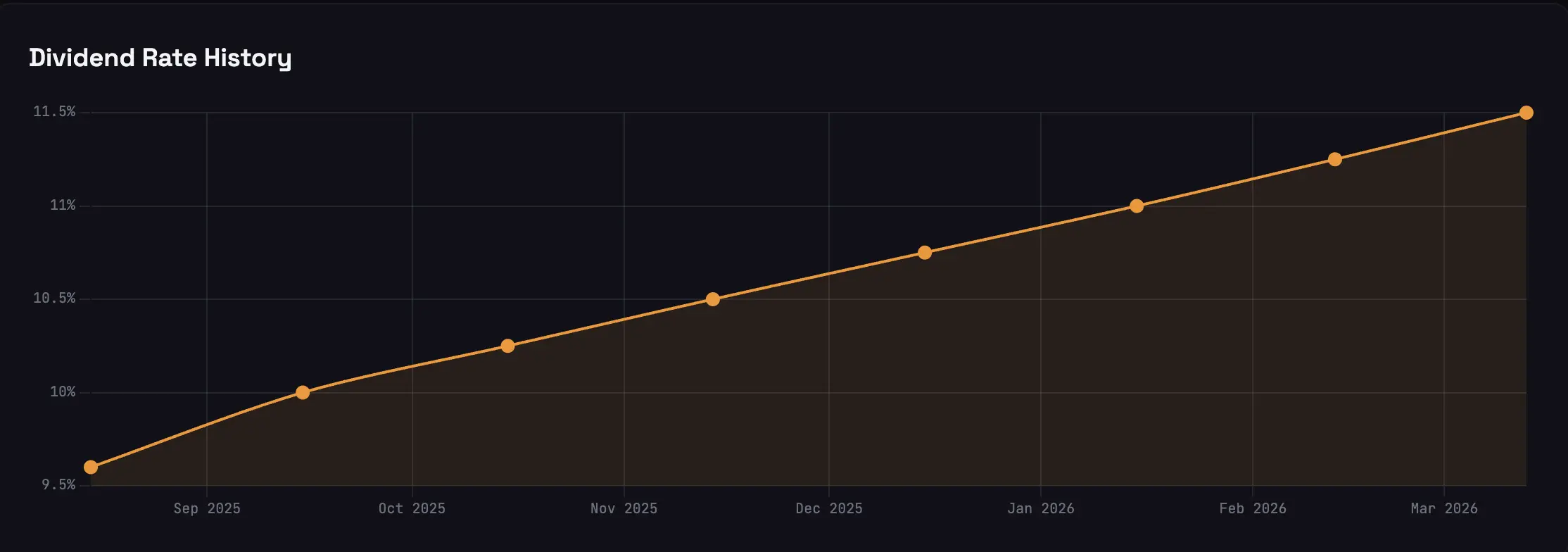

To enhance STRC’s appeal, Strategy has made eight dividend adjustments, raising the annualized yield from 9.6% to 11.5%. Compared to traditional high-yield assets like high-yield bonds, deposits, and money market funds, which generally hover around 4% to 6%, STRC’s fixed income returns are more competitive.

These features make STRC more attractive to buyers. For most traditional funds, Bitcoin’s volatility is too high, lacking cash flow and not fitting asset allocation frameworks; MSTR adds premium and leverage, offering higher yield elasticity but also amplifying risks. Previously, several U.S. public pension funds experienced significant paper losses holding MSTR.

In contrast, STRC offers a more acceptable compromise: Bitcoin as the underlying asset, near-par pricing, and stable, predictable monthly cash flows. Additionally, the preferred stock structure ranks higher than common stock in liquidation, providing some safety margin.

The launch of STRC also reflects a shift in Strategy’s financing logic.

As MSTR’s premium narrows, the Bitcoin flywheel driven solely by issuing common stock has hit a bottleneck. Strategy previously even promised not to issue common stock easily when mNAV is below 2.5 times.

STRC has become a “new magic” for Strategy to maintain Bitcoin accumulation speed in a bear market. But problems also arise: preferred stocks entail fixed dividend payments. Expanding STRC scale alone would directly increase leverage.

To address this, Strategy employs a dual ATM approach—one with more volatility but higher potential (common stock), and the other with stable, high dividends (preferred stock). By issuing both STRC and MSTR simultaneously, it raises funds to buy Bitcoin while replenishing equity capital, controlling leverage as the asset scale expands. When this financing mechanism operates continuously, STRC absorbs liquidity from the fixed-income market, giving Strategy a relatively independent ongoing buy-in outside the crypto cycle.

However, high dividends come with costs. The latest STRC issuance added about $135 million annually in dividend burden, with Strategy’s annual dividend expenditure now exceeding $1.08 billion. Although Strategy has about $2.25 billion in cash reserves to cover at least two years of dividends, pressure remains.

If Bitcoin prices remain stagnant long-term, and STRC must keep raising yields to stay attractive, financing costs will continue to rise, gradually squeezing space. The repeated dividend hikes indicate an ongoing need for increased incentives.

Nevertheless, STRC is unlikely to experience a UST-style collapse. It does not have on-chain automatic liquidation, flash loan runs, or instant redemption mechanisms. It remains a traditional credit product issued by Strategy, with all adjustments (like dividend increases or delayed payments) controlled actively by the company. Its underlying support is Bitcoin, not infinitely dilutable tokens. This means that even in extreme scenarios, risks are more likely to manifest as slow bleeding.

Overall, STRC has successfully opened a channel to convert traditional fixed-income capital into Bitcoin spot demand. While the sustainability of its high-yield model remains to be seen, this new flywheel has already started turning.

Related Articles

NYSE Welcomes Morgan Stanley’s MSBT Launch as First Spot Bitcoin ETF Issued by a Major US Bank

Bank-backed bitcoin ETFs are accelerating institutional adoption and strengthening market credibility. The NYSE marked a new milestone as Morgan Stanley Investment Management rang the closing bell and celebrated the launch of MSBT, which the NYSE described as the first spot bitcoin ETF by a major

Coinpedia3h ago

BTC falls 0.49% in 15 minutes: fragile long leverage and active sell-off pressure resonate to weigh on the short term

From 18:00 to 18:15 (UTC) on 2026-04-17, the BTC price fluctuated and trended downward within the 77097.4 to 77573.2 USDT range. Over these 15 minutes, the return rate recorded -0.49%, and the amplitude reached 0.61%. During this period, market trading was active; short-term volatility was amplified, and trading attention increased significantly. The main driver behind this abnormal move is that the overall leverage structure is bearish and long positions are fragile. At present, the BTC perpetual contract funding rate has remained negative for 11 consecutive days, indicating that the bears have the upper hand in the market. In addition, futures open interest (OI) is about 628.3 billion USDT, which is at a historical high. During the anomaly window, trading volume increased noticeably. On-chain data shows large amounts of BTC flowing from long-term holder addresses to exchanges, suggesting that active sell orders may have triggered longs to passively reduce positions, amplifying downward price pressure. Moreover, institutional positioning enthusiasm in the mainstream contract market has cooled off; liquidity boundaries have tightened, causing large-trade activity to have an amplified effect on market volatility. In the options market, implied volatility rose to 39.81%, increasing demand for downside protection and reflecting a defensive posture among market participants. Macro-environment volatility and some capital flowing into safe-haven assets, together with the recent regulatory uncertainty-related historical events, reinforced the move, pushing overall market risk appetite lower. Current BTC leverage risks still remain. If, in the future, there are concentrated sell-offs, volatility may be further amplified. It is recommended to continue monitoring sustained high OI levels, the persistence of negative funding rates, and on-chain transfers of large amounts of funds, and to stay alert for whale behavior and any disruptions to market sentiment caused by macro-policy developments. For subsequent price action, please watch key support levels, institutional and whale on-chain moves, and relevant global market news, and guard against short-term risks.

GateNews4h ago

Bitcoin Liquidations Hit $815M as BTC Surges Above $78K Amid Iran Strait Opening

Over $815 million in leveraged cryptocurrency positions were liquidated recently, mainly due to short positions against Bitcoin. Markets improved as Iran reopened the Strait of Hormuz and Trump hinted at a deal with Iran, boosting Bitcoin prices significantly.

GateNews5h ago

Cardano Founder Hoskinson Warns BIP-361 Could Freeze 1.7M Bitcoin

Charles Hoskinson warned that Bitcoin's BIP-361 upgrade, meant to address quantum threats, is wrongly classified as a soft fork. It could freeze 1.7 million BTC, including 1 million from Satoshi Nakamoto, as early coin owners can't prove ownership.

GateNews5h ago

BTC drops 0.45% in 15 minutes: Whale concentrated transfers into exchanges stack up sell pressure while leverage withdrawals amplify the pullback

From 17:00 to 17:15 (UTC) on 2026-04-17, BTC saw a brief drop. The return rate recorded was -0.45%, with the price ranging from 77354.3 to 77916.9 USDT and a swing of 0.72%. During the event, market attention warmed up, volatility intensified, and spot market liquidity changed significantly.

The main driver of this price anomaly was that whale wallets concentrated transfers to exchanges. In a single 15-minute period, the exchange inflow surged to 11,000 BTC, reaching a new high since December 2025. The average amount deposited per transaction was as high as 2.25 BTC, indicating that large holders chose key price levels to concentrate and release their positions, clearly lifting sell pressure. At the same time, BTC futures open interest fell to a 14-month low of $841 million, as leverage funds exited sharply. The spot market’s pull on price fluctuations became the main factor, further magnifying the impact of whale trading.

In addition, although ETF funds had a net inflow with a hedging effect—bringing the April cumulative inflow to $5.651 billion—within this anomaly window they were not able to fully absorb large sell orders. The spot market mainly relied on institutional buying to digest the selling pressure, and overall risk appetite contracted. On-chain data shows that 41% of the BTC supply is in a loss-making range, and some holders who bought at lower prices face take-profit and stop-loss pressure. With multiple factors converging, short-term tension formed among exchange inflows, leverage withdrawal, profit realization, and institutions’ ability to absorb, increasing the magnitude of spot volatility.

Short-term risks are worth watching closely. Users should closely monitor core indicators such as the subsequent exchange inflow volume, the pace of ETF net inflows, and futures open interest. If whale sell orders still have not eased and ETF inflows cannot accelerate in step, the BTC price may remain under sustained pressure. Users should focus on on-chain transfers and changes in major holders’ positions, watch the spot market’s key support ranges and trading structure, obtain more market information in a timely manner, and stay alert to risks brought by sharp volatility.

GateNews5h ago