Why Stablecoins Are Set for Revaluation in 2026

If the core consensus in the crypto market over the past few years was “Bitcoin is a store of value, Ethereum is an application platform,” then by 2026, a new and increasingly clear consensus is taking shape: stablecoins are becoming the standard unit of settlement for on-chain financial systems.

This wave of revaluation is driven by three consecutive shifts.

Regulatory Uncertainty Has Significantly Decreased

In July 2025, U.S. President Trump signed the stablecoin regulatory bill—the GENIUS Act. For the industry, this marks the first time the U.S. has established a clear regulatory framework for USD stablecoins, focusing on reserve assets, consumer protection, and issuance constraints. Simultaneously, in April 2025, the SEC issued a statement regarding certain stablecoins, clarifying that, under specific conditions—when used for payments and as a store of value, and fully backed by low-risk, highly liquid assets—issuance and redemption do not constitute securities issuance. While not a blanket approval for all stablecoins, this has greatly clarified compliance boundaries for the market.

Institutions No Longer View Stablecoins as a Marginal Experiment

In June 2025, Stripe announced support for Shopify merchants to accept USDC payments, with settlements defaulting to local fiat. At the end of 2025, Visa rolled out a stablecoin settlement framework in the U.S., enabling institutions to settle on a 7-day cycle and disclosing annualized stablecoin settlement volumes reaching $3.5 billion. These moves send a clear message: stablecoins are no longer just a medium for crypto-native transfers—they're entering traditional payment networks and institutional clearing processes.

Asian Markets Are Completing the Regulatory Puzzle

In 2025, Hong Kong enacted the Stablecoin Ordinance, bringing fiat-referenced stablecoin issuance under a licensing regime and requiring issuers to meet standards for reserve management, redemption, auditing, and anti-money laundering. As of April 2026, the Hong Kong Monetary Authority’s public register still showed “no licensed stablecoin issuers,” reflecting higher entry standards rather than regulatory retreat. The significance for the market isn’t the number of licenses issued in the short term, but that Hong Kong provides a regulatory blueprint for the Asian stablecoin sector.

The reason stablecoins have become the “strongest narrative” in 2026 isn’t novelty—it’s that, for the first time, they’ve achieved policy confirmation, institutional validation, and integration into real commercial scenarios.

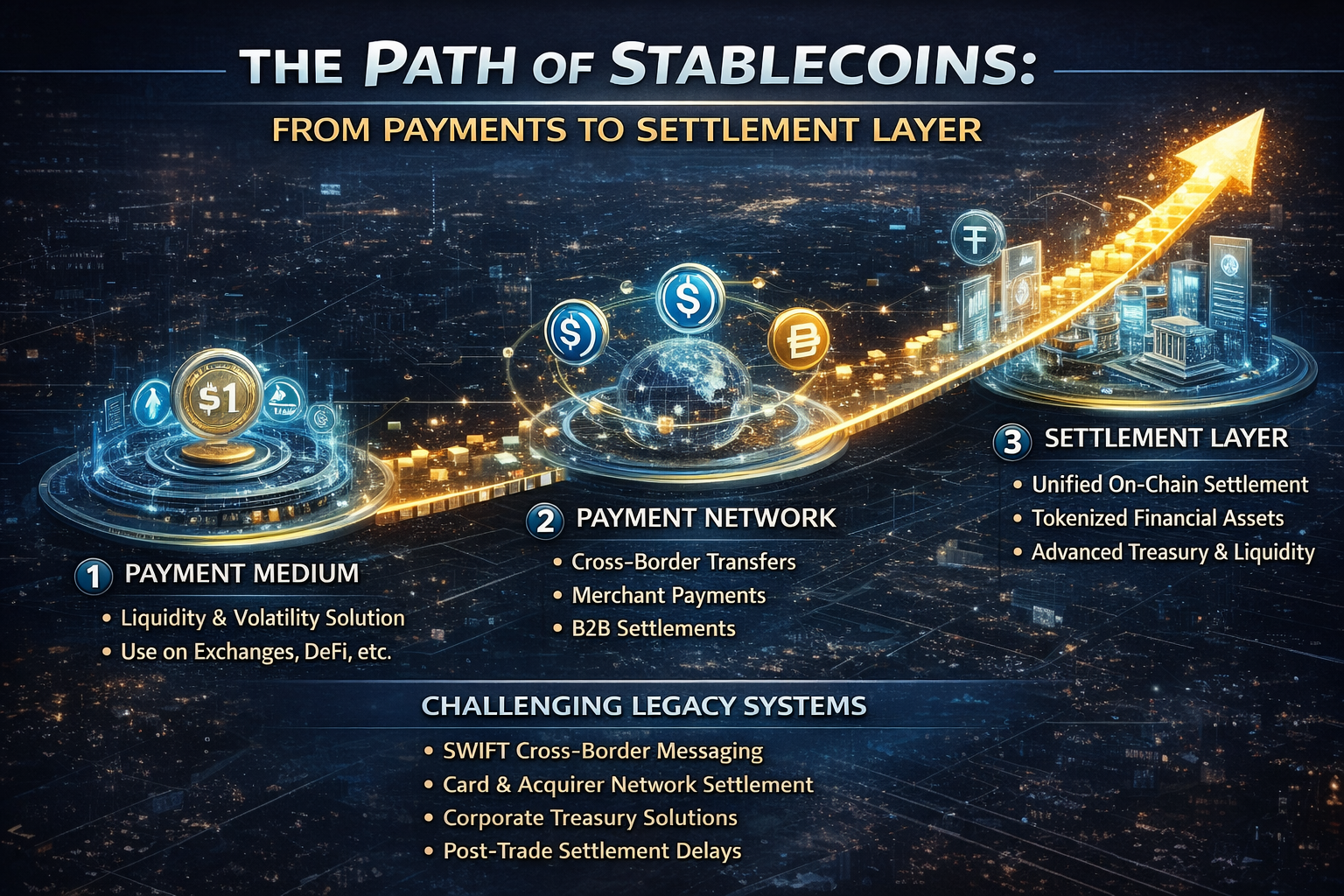

Many still see stablecoins as “on-chain digital cash,” but that’s only the first layer.

From a functional perspective, stablecoins have evolved through three main stages:

-

Stage 1: Transaction Medium The earliest stablecoins were primarily used for exchange pricing, arbitrage, hedging, and capital parking—addressing crypto market volatility and inefficient fiat on/off-ramps.

-

Stage 2: Payment Tool As on-chain transfer costs fell, wallet infrastructure matured, and payment companies integrated stablecoins, they began to serve cross-border transfers, merchant payments, and B2B settlements—moving closer to the real economy.

-

Stage 3: Settlement Layer This is the most significant upgrade in 2026. The “settlement layer” is not just moving money—it enables asset delivery, trade settlement, inter-institutional reconciliation, and on-chain credential flow on a unified ledger, representing a higher tier of financial infrastructure.

Why is the settlement layer so critical? Because payments only solve “how funds arrive,” while settlement addresses “when a transaction is final, how credit is delivered, and how funds are confirmed in real time.” In traditional finance, payments and settlement are often handled by separate systems, with cross-border scenarios further complicated by correspondent banks, time zones, and settlement delays. Stablecoins’ appeal is in compressing these fragmented steps into a much shorter pathway.

Viewed this way, stablecoins’ real competition may not be other crypto assets, but:

-

SWIFT-style cross-border messaging systems

-

Certain settlement processes of card networks and acquiring banks

-

Internal cross-border treasury systems for enterprises

-

Delayed confirmation in post-trade settlement

This is why, as more institutions discuss stablecoins, the focus is shifting from “payments” to settlement, treasury, and liquidity management.

Who Drives Stablecoin Expansion: Regulation, Institutions, and On-Chain Assets

Stablecoin momentum isn’t the result of any single issuer—it’s the product of multiple forces converging.

1. Regulation Is Turning “Gray Innovation” Into “Regulated Financial Instruments”

Regulatory moves in the U.S. and Hong Kong show that mainstream markets have accepted reality: stablecoins are here to stay, and it’s better to regulate them than allow unchecked growth.

This has changed the industry in key ways:

-

Compliant issuers now enjoy a credit premium

-

Reserve transparency is a core competitive edge

-

Redemption capability and user protection are shaping market share

-

Competition is shifting from pure liquidity to a mix of “regulation + channels + network”

2. Payment and Financial Infrastructure Providers Are Entering the Market

Stripe and Visa represent two distinct strategies:

Stripe expands use cases; Visa raises the credibility of financial infrastructure. When both advance in parallel, stablecoins’ network effect will extend from the crypto sphere to the broader internet economy.

3. On-Chain Asset Expansion Demands Stablecoins as a Unified Settlement Unit

In recent years, stablecoin demand was driven mainly by trading. In 2026, true growth potential lies in RWA, on-chain government bonds, tokenized funds, on-chain lending, and institutional asset transfers. The reason is simple: as more real-world assets move on-chain, the market needs a settlement unit with low volatility, deep liquidity, and cross-platform usability—stablecoins are the natural choice.

In other words, stablecoins aren’t just a sidekick for RWA—they may be the precondition for a closed-loop tokenized asset market.

The Most Compelling Stablecoin Beneficiaries

If stablecoins continue to strengthen their “settlement layer” role in 2026, the biggest beneficiaries won’t be issuers alone.

Attention should shift to the infrastructure layer supporting stablecoin liquidity and settlement:

-

Compliant Issuance and Custody: Market share will increasingly concentrate among platforms with transparent reserves, regulatory compliance, and robust redemption capabilities.

-

Payment Access: Including merchant payments, wallet aggregation, fiat on/off-ramps, subscription payments, and cross-border settlement APIs.

-

Interchain Liquidity and Cross-Chain Transfers: As stablecoins circulate across multiple chains and layer 2s, cross-chain settlement and liquidity coordination become critical.

-

Institutional Settlement and Treasury Management: Banks, brokers, payment companies, and multinationals need new stablecoin-based treasury and risk control systems.

-

RWA and On-Chain USD Yield Products: As stablecoins become the foundational settlement layer, on-chain government bonds, cash management, and yield products will expand rapidly.

In short, stablecoins aren’t just a point opportunity—they’re the foundation of an entirely new financial services value chain.

The Strongest Narrative Still Carries Risks

Even with stablecoins’ growing dominance in 2026, risks remain.

Key risks include:

-

Regulatory Fragmentation: Divergent rules across the U.S., Hong Kong, Europe, and offshore markets could fragment stablecoin liquidity by jurisdiction.

-

Centralization Risk: Most major stablecoins rely on centralized issuers, custodian banks, and freeze permissions, meaning they’re not fully trustless assets.

-

Reserve and Redemption Stress Tests: In extreme conditions, whether stablecoins can continue to offer sufficient, fast, and low-friction redemption remains an open question.

-

Yield Conflicts and Business Model Constraints: Per the SEC, stablecoins with “payment-type” features shouldn’t promise holders interest, profits, or governance rights. This limits “high-yield” marketing and means future winners can’t rely solely on subsidies.

Thus, the strongest stablecoin narrative doesn’t mean endless hype like meme coins. It’s a classic infrastructure story: the pace may be steadier, but once standards are set, the moat is much deeper.

Conclusion: Stablecoins Are Becoming the Core Interface of New Financial Infrastructure

Looking back, the most important change for stablecoins in 2026 isn’t another supply record or a spike in issuer valuations—it’s that the market is finally recognizing: the endgame for stablecoins isn’t just a “better digital dollar,” but a unified interface connecting payments, trading, settlement, and asset movement.

This is why the “payment tool to settlement layer” evolution is so pivotal. Payments solve efficiency; settlement solves the core of financial infrastructure. The former means usability, the latter means irreplaceability.

For the crypto market, stablecoins are poised to be 2026’s strongest narrative—not just because they’re hot, but because, for the first time, they meet three critical conditions:

-

Real-world demand

-

Regulatory support

-

Network effects

When a sector moves beyond serving only crypto trading and starts enabling global capital flows, its narrative reaches a new level.